So you thought the “Crowding Out Effect” and “Phillips Curve” Were Long Gone

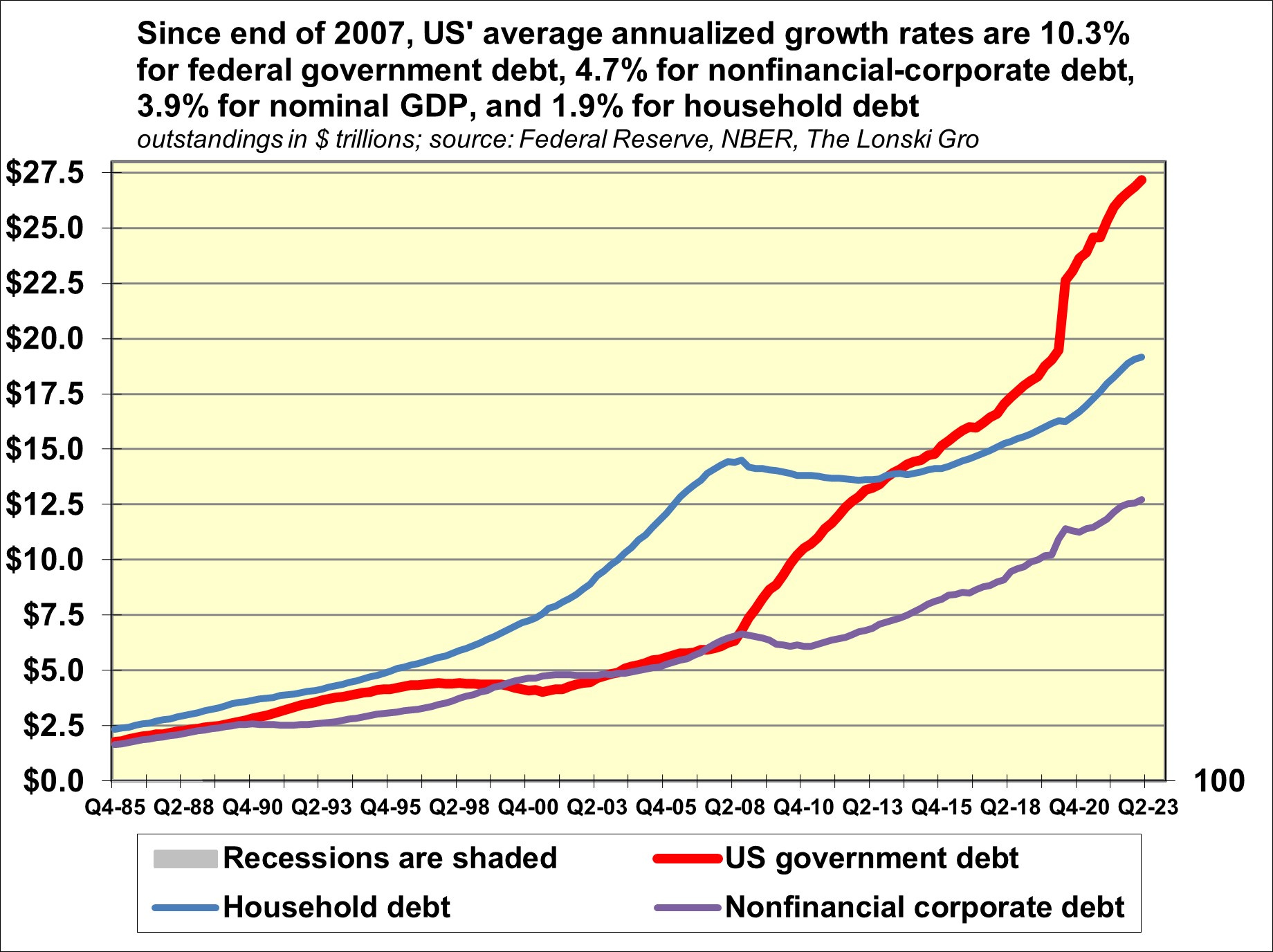

The Great Recession was largely the consequence of too much household debt. The next recession will probably be viewed as the offshoot of excessive US government indebtedness.

It is not beyond the realm of a possibility that the nearly $1 trillion of US government borrowing expected for the current quarter may push Treasury bond yields up to heights that roil financial markets and curb private-sector spending. If the “crowding out effect” were to return, the political opposition to increased federal spending and more regulations will be mighty enough to force Washington into reversing course.

Could it be that whoever is running the federal government may have to re-think the Chips Act, the Inflation Reduction Act, and social security? Perhaps Washington has overextended itself with prospective subsidies for the domestic manufacture of micro-chips, green energy, and electric vehicles? Also, let us not overlook the many federal regulations that will follow from forthcoming subsidies.

Heightened government intervention sullies inflation outlook …

Not only do prospective federal subsidies and regulations add to federal borrowing needs, but they also will help to stoke price inflation. Given July’s already historically low 3.5% unemployment rate, a massive influx of government intervention will accelerate wage growth. However, at a significantly higher jobless rate, added government intervention will be less of a propellant to wage growth.

The impetus behind faster wage-driven consumer price inflation will be reinforced by the loss of efficiency to the expanded federal regulation of labor practices for those companies receiving federal subsidies. Even employers not receiving subsidies will face higher labor costs than otherwise as the expanded role of government in the labor market puts upward pressure on employee compensation.

Faster wage growth may enliven inflation …

Complacency on labor costs is unwarranted. Earlier optimism regarding disinflationary wage growth stemmed from a deceleration by the average monthly increase for the private-sector’s average hourly wage from the 0.4% of 2022’s second half to the 0.3% of 2023’s first quarter. However, the average hourly wage subsequently grew by 0.4% per month, on average, during April-July 2023.

Moreover, July’s 4.4% year-to-year increase by the average hourly wage of private-sector workers was well above 2017-2019’s 3.0% average that overlapped a 1.8% average annual rate of core PCE price index inflation.

UPS and UAW say it’s too early to dismiss faster wage growth …

Wherever you look, workers are demanding significantly higher wages. The UPS’ generous labor agreement will serve as a benchmark.

The UAW wants a 40% increase over four years, or 10% per annum, from the US’ big three automakers. Others are looking for double-digit percent wage hikes.

Though actual annual wage increases may fall short of 10%, they are likely to climb above 5% if a tight labor market persists. So much for the containment of inflation expectations. Wage growth can only benefit from the recent waning of recession fears.

Barring the attainment of a significantly faster labor productivity growth, the avoidance of persistently rapid price inflation requires private-sector wage growth no greater than 3% annually.

In order to quell wage pressures, the now 3.5% unemployment rate needs to climb above 4%. And a greater than 4% jobless rate by mid-2024 would be consistent with a recession. A labor market recession is the most likely means of realizing a disinflationary softening of the job market.

A rejuvenation of expenditures will accelerate price growth. A soft landing will decelerate price inflation only if spending slows. But a slowing of expenditures may be impossible if, as feared, wage growth gains speed.

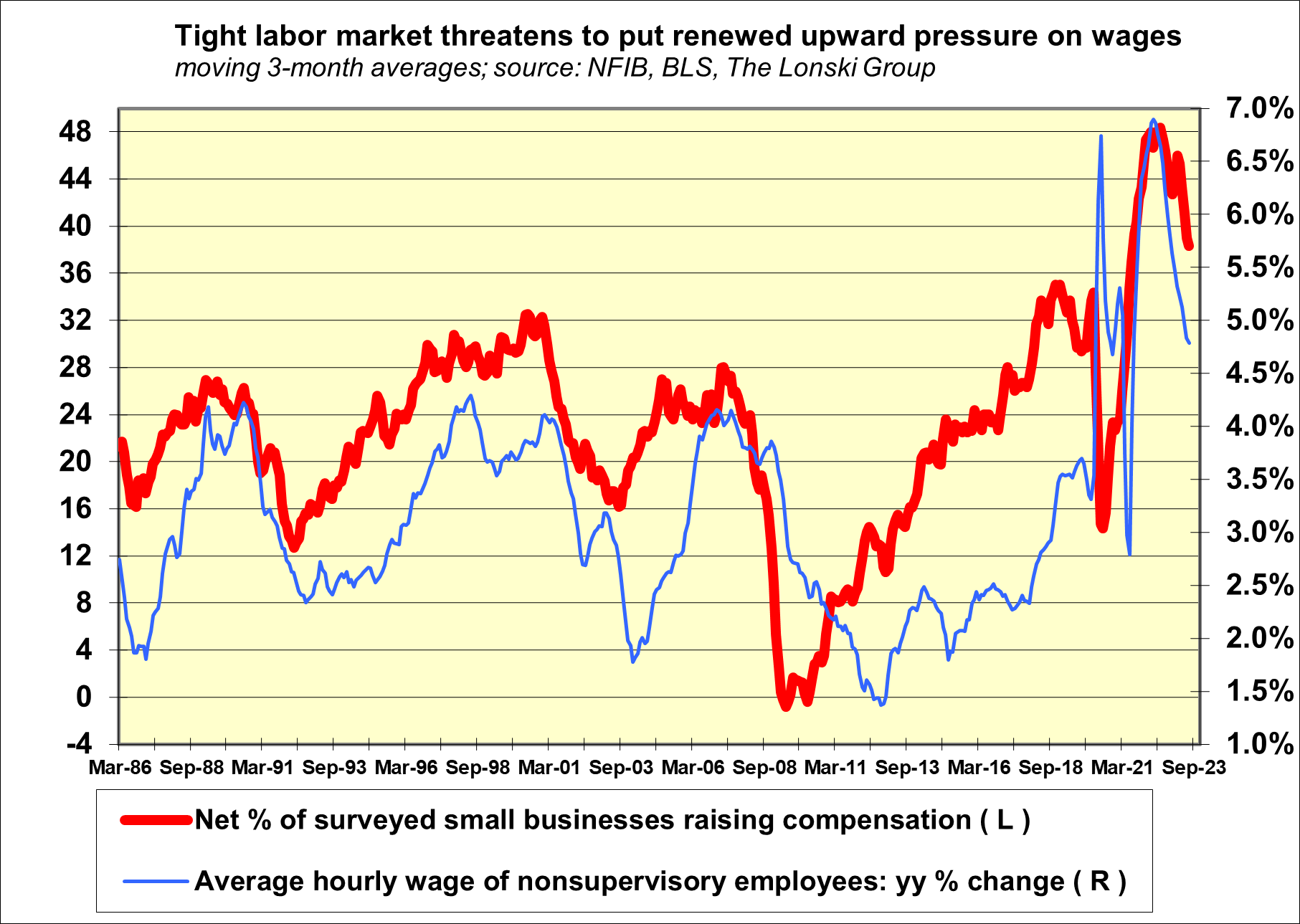

Small businesses still face wage pressures …

The NFIB’s net percent of surveyed small businesses increasing employee compensation edged up from June 2023’s +36 percentage points to July’s +38 points. When the average hourly wage of all private-sector employees grew by 3.0% annually, on average, during 2017-2019, the small-business wage hike index averaged +30 points.

This index of wage pressures facing small businesses set a record high at the +50 points of January 2022.

Rate cuts may strengthen the case for impending recession …

Thus far in August, the 10-year Treasury yield has remained above 4%. August’s month-long average for the benchmark Treasury yield might yet be the highest since the 4.10% of December 2007. Coincidentally, the latter was the first month of the Great Recession.

Nevertheless, the start of each of the four recessions since 1982 occurred amid a declining trend for the federal funds rate.

In other words, the Fed had already started a series of rate cuts before recession arrived.

The duration of rate cuts prior to recession’s arrival ranged from a low of two months prior to the March 2001 start of 2001's recession to a high of 13 months prior to the July 1990 start to 1990-1991’s downturn. The median span between the peaking of fed funds and the start of a recession was 5.5 months.

Thus, if the Fed begins to cut rates during early 2024, a recession might arrive by mid-year. Here, an election year recession would reduce the incumbent party's chances of staying in power.

In turn, the fate of existing subsidy and regulatory programs will become more uncertain. Business spending plans may suffer.

Plunge by homebuyer mortgage applications doesn’t jibe with housing strength …

Some say higher Treasury bond yields don’t matter. But then why were July’s mortgage applications from potential homebuyers down by -24% year-on-year? One obvious culprit is the dearth of existing homes for sale.

Existing homes for sale are in short-supply for a number of reasons. They include (i) the above-average risk of home price deflation that is implicit to a historically high ratio of home prices to income, (ii) the unwillingness to give up the 3.8% average mortgage rate of the 10 years ended 2021 for a now nearly 7% mortgage rate, and (iii) the lack of attractive job opportunities that might otherwise prompt housing turnover via relocation or substantially higher salaries. Seldom has a 3.5% unemployment rate looked so limp.

How to tell when the job market is knocking on recession’s door …

July’s jobs report supplied little, if any, evidence of an impending recession. Often, recessions are preceded by a notable shrinkage of jobs growth and a rising unemployment rate.

The labor market would signal either an impending or ongoing recession if (i) the moving three-month average change of payrolls is no greater than 100,000 new jobs per month, (ii) the unemployment rate’s moving three-month average rises from July 2023’s 3.65% to 4%, and (iii) the annualized quarterly contraction for private-sector hours of work is deeper than -0.2%. During the three-months-ended July, payrolls grew by 218,000 jobs per month, on average, while private-sector hours rose by 0.6% annualized from the three-months-ended April 2023.

International trade data implies world economy is in sad shape …

Shrinkages of world trade often are the product of global economic downturns. China’s export-dependent economy has been hit hard by deep year-on-year declines by exports. The yearly plunge by China’s exports deepened from June’s -12.4% to July’s -14.5%. The latter included a -23.1% year-on-year plunge by China’s exports to the US.

Meanwhile, the yearly percent drop by China’s imports worsened from June’s -6.8% to July’s -12.4%. Import contraction brings attention to China’s lackluster domestic spending. Currently, there is no such thing as a middle-class consumer spending boom in China.

As inferred from China’s shallower year-over-year setbacks of -5.0% for exports and -7.6% for imports for 2023’s first seven months, China’s trade performance has deteriorated from what held earlier in 2023.

US exports and imports contracted together in only 6 of last 73 years …

US trade data also are weak. The year-on-year percent change for US exports sank from Q1-2023's 8.4% advance to Q2-2023's -2.9% contraction.

Moreover, US imports year-on-year shrinkage deepened from Q1-2023's -1.6% to Q2-2023's -6.4%. The worsened performance by US imports suggests US domestic spending slowed from the first to the second quarter.

Calendar-year 2023 may show the first simultaneous declines by US exports and imports since 2020’s COVID recession year. Previous calendar year declines by the US' exports and imports occurred in 2016, 2015, 2009, 1982, and 1949. The latter three years overlapped recessions.

Surveyed small businesses report recessionary sales trend …

According to a NFIB survey, the net percent of polled small businesses reporting an increase in sales comparing the three-months-ended July 2023 with the contiguous three-months-ended April 2023 sank to -13 percentage points. So deep of a negative reading ordinarily occurs during recessions.

Around the start of the COVID recession, the index sank from March 2020's +8 points to April's -11 points. Amid 2017-2019’s relative economic calm, the small business sales index averaged +5 points.

July’s vehicle sales favor smaller rise by real consumer spending …

The seasonally adjusted and annualized pace for new cars and light trucks sold in the US rose by 0.5% monthly to 15.7-million units. However, the latter was -8.7% under 2017-2019’s average annual sales rate of 17.2-million units.

The drop by the monthly increase for unit sales of light motor vehicles from June’s 4.0% to July’s 0.5% is consistent with an expected slowing by the monthly increase of all real consumer spending from June’s 0.4% to 0.2% in July.